Capital Gains Tax (CGT)- Withholding tax- prepayment CGT

0

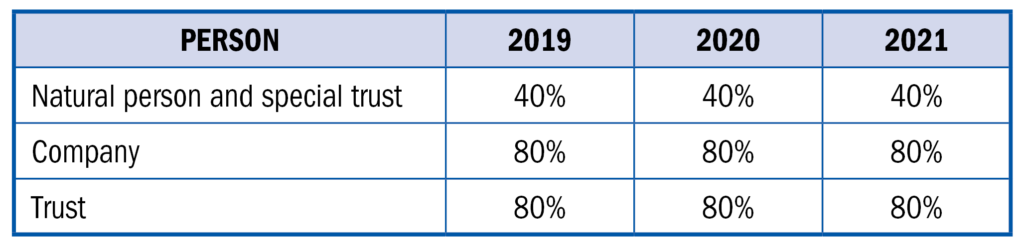

The purchaser must withhold CGT on the purchase price where assets are purchased from a non-resident except where the amount payable by the purchaser is less than R2 million. This withholding tax is not a final tax and is merely a prepayment of the expected CGT. The following withholding tax rates are applicable and are based on the proceeds on disposal: